RCM Education for Executive Leadership: What Every CEO, CFO, and COO Needs to Know About Revenue Cycle

Join us for an executive-level webinar featuring Cissy Mangrum, MBA, CMPE, CPC, CDC, nationally recognized healthcare operations strategist and revenue cycle authority, as she shares what every CEO, CFO, and COO needs to know about revenue cycle—but was never told.

Revenue cycle is no longer just an operational function.

Webinar Event

July 9, 2026

3:30 PM CDT

In today's healthcare environment, it's a strategic growth driver—and one of the biggest blind spots for executive leadership.

As patient financial responsibility continues to rise, many organizations are making critical business decisions without full visibility into where revenue is leaking, where patients are falling out of the process, and how financial friction is impacting growth.

Join us for an executive-level webinar featuring Cissy Mangrum, MBA, CMPE, CPC, CDC, nationally recognized healthcare operations strategist and revenue cycle authority, as she shares what every CEO, CFO, and COO needs to know about revenue cycle—but was never told.

What You'll Learn

Where revenue is leaking—and why it's often invisible at the executive level

How rising patient responsibility is changing the economics of care

Why traditional revenue cycle metrics don't tell the full story

What high-performing organizations are doing differently to improve cash flow, patient experience, and sustainable growth

Meet the Speaker

With more than 25 years of experience and having worked alongside 2,700+ physicians and healthcare providers, Cissy Mangrum, Co-Founder and Chief RCM Officer at RevTech Partners, has helped organizations optimize operations, improve financial performance, and create exceptional patient experiences. Cissy is known for helping healthcare leaders uncover hidden opportunities within their revenue cycle that drive measurable business growth.

The Hidden Revenue Already in Your Practice: Reactivating Patients Who Said "Not Yet"

Every practice has them—folders full of consultations that never converted. Patients who seemed genuinely interested, who asked thoughtful questions, who left saying they'd "think about it" or "call back soon." Weeks became months. Months became years. Those patients represent procedures that were wanted but never scheduled, treatment plans that were presented but never accepted, revenue that was almost captured but ultimately lost.

Most practices treat these unconverted consultations as closed files. The patient said no, and that's that. But here's what a decade of working with healthcare practices has taught the team at Alphaeon Credit: most of those patients didn't actually say no. They said "not yet." And "not yet" is a very different answer—one that often converts to "yes" when the circumstances change.

Understanding Why Patients Delay

Before attempting to reactivate past consultations, it helps to understand why patients delay in the first place. The reasons fall into several categories, and each suggests a different reactivation approach.

Financial timing was wrong. The patient wanted the treatment but couldn't fit it into their budget at that moment. Maybe they'd just paid holiday expenses, covered an unexpected car repair, or hadn't yet received their tax refund. The desire was real; the timing wasn't. These patients are often excellent reactivation candidates because their underlying interest hasn't changed—only their financial circumstances have.

They needed time to decide. Some patients genuinely need to process major decisions, especially for elective procedures with significant costs. What felt overwhelming at the consultation may feel more manageable after reflection. The patient who left uncertain may now feel ready—but won't reach out unless prompted.

Life got in the way. A family emergency, a job change, a health issue, or simply the chaos of daily life pushed the procedure off the priority list. These patients often still want the treatment and feel guilty about not following through. A well-timed, non-judgmental outreach can move them back toward action.

They found the cost barrier insurmountable. If financing wasn't presented effectively—or wasn't presented at all—patients may have concluded they simply couldn't afford the procedure. They left believing the door was closed when it actually wasn't.

The Cost of Ignoring Past Consultations

Practices invest significantly in generating new patient consultations. Marketing, advertising, referral programs, community presence, online reputation management—all of these efforts aim to get prospective patients through the door. When those consultations don't convert, that investment yields no return.

But the cost goes beyond wasted marketing dollars. Every unconverted consultation represents:

The time clinicians spent evaluating the patient and developing treatment plans

The administrative time spent scheduling, confirming, and documenting the visit

The opportunity cost of that appointment slot, which could have held a converting patient

The potential lifetime value of a patient relationship that never developed

When practices successfully reactivate even a fraction of past consultations, the return on that effort is remarkably high. These patients require no new marketing spend. They've already been evaluated. Treatment plans already exist. The heavy lifting is done—all that remains is removing whatever barrier prevented them from proceeding.

Building a Reactivation System

Effective reactivation isn't about making one desperate phone call to old contacts. It requires a systematic approach that respects patients while creating genuine opportunities for reconnection.

Start with segmentation. Not every past consultation deserves the same approach. Patients who consulted last month are different from those who consulted two years ago. Patients who expressed strong interest but cited cost concerns are different from those who seemed ambivalent about the treatment itself. Segment your unconverted consultations by recency, stated reason for delay, treatment type, and any other relevant factors.

Lead with value, not sales pressure. The worst reactivation approach is a message that essentially says "you didn't buy from us before, please buy now." Instead, lead with something genuinely useful. Has something changed that's relevant to their situation? New technology? New financing options? New research supporting the procedure they considered? Give them a reason to re-engage beyond just "we want your business."

Make it easy to restart. Patients who delayed once may feel awkward about returning. They might worry about judgment, about having to re-explain their situation, about starting the whole process over. Assure them that their records are on file, that they're welcome back whenever they're ready, and that the path forward is simple.

Present financing proactively. If cost was a barrier—stated or suspected—the reactivation message should address it directly. "We now offer flexible financing options that make treatment more accessible" or "Many patients are surprised to learn they can begin treatment for monthly payments that fit their budget" opens doors that patients may have assumed were closed.

The Financing Conversation, Take Two

For patients whose original consultation predates your practice's current financing offerings—or whose experience didn't include a strong financing presentation—reactivation provides a second chance to have that conversation correctly.

This is particularly relevant for practices that have upgraded their financing programs. If you previously offered single-tier financing that declined patients with less-than-perfect credit, and you now offer multi-tier options with broader approval, those previously declined patients deserve to know. The patient who was told "no" two years ago may receive a "yes" today.

Even patients who weren't formally declined may benefit from a refreshed financing conversation. Perhaps financing was mentioned but not emphasized. Perhaps monthly payment options weren't calculated specifically for their treatment plan. Perhaps they didn't realize how accessible their desired treatment could be.

Reactivation outreach that specifically highlights financing—"We're reaching out because we've expanded our payment options and wanted to make sure you knew about them"—addresses cost barriers directly while giving patients a face-saving reason to reconsider.

Timing Reactivation Strategically

Certain moments create natural opportunities for reactivation outreach.

After major financial events. Tax season, bonus seasons, and the start of new insurance years create windows when patients may have more financial flexibility or motivation to use benefits before they expire.

When something changes at your practice. New technology, new providers, new services, expanded hours, or new financing options all provide legitimate reasons to reach out. "We wanted to let you know about some changes that might be relevant to the treatment we discussed" feels helpful rather than pushy.

At natural decision points. The approach of a new year prompts reflection and resolution-making. Patients who've been putting off treatment may be more receptive to outreach in late fall or early winter.

Before life milestones. If you know a patient was considering treatment before a specific event—a wedding, reunion, major birthday—outreach that references adequate lead time can be effective. "We know you mentioned wanting to address this before your daughter's wedding, and we wanted to reach out with enough time to ensure you'd be completely healed."

What Reactivation Messages Should Include

Effective reactivation outreach includes several key elements:

Acknowledgment of time passed. Don't pretend the gap didn't happen. A simple "It's been a while since we last spoke" acknowledges reality and avoids awkwardness.

No guilt or pressure. Patients delayed for their own reasons. Making them feel bad about it guarantees they won't respond. Keep the tone warm and welcoming.

A reason for reaching out. Give them something specific—new options, relevant timing, an update they'd want to know about. Random "just checking in" messages feel like sales calls.

Easy next steps. Tell them exactly what to do if interested. Call this number, reply to this email, click this link. Remove all friction from re-engagement.

Financing information when appropriate. If cost was a known or likely barrier, address it explicitly. Let them know affordable options exist.

Measuring Reactivation Success

Track reactivation efforts separately from general marketing to understand their true return. Relevant metrics include:

Response rate to reactivation outreach

Consultation reconversion rate (reactivated patients who schedule follow-up)

Procedure completion rate among reactivated patients

Average case value of reactivated patients

Cost per reactivated case (typically minimal compared to new patient acquisition)

Most practices find that reactivated patients convert at higher rates and require lower investment than entirely new prospects. This makes reactivation one of the most efficient revenue-generating activities a practice can undertake.

Start Recovering Lost Revenue Today

Your practice already has a database of patients who wanted treatment but didn't proceed. That database represents real revenue waiting to be recovered—revenue that requires no new marketing spend, no new consultations, and minimal administrative effort.

Alphaeon Credit helps practices not only convert new consultations but also reactivate past ones. With multi-tier financing that approves patients across the credit spectrum, competitive terms that make treatment accessible, and staff training resources that help teams present financing confidently, practices using Alphaeon consistently capture cases that would otherwise remain lost.

Contact Alphaeon Credit at 1-920-306-1794 or email teamcredit@alphaeon.com to learn how flexible financing can help your practice recover revenue from patients who said "not yet"—and turn them into patients who say "yes."

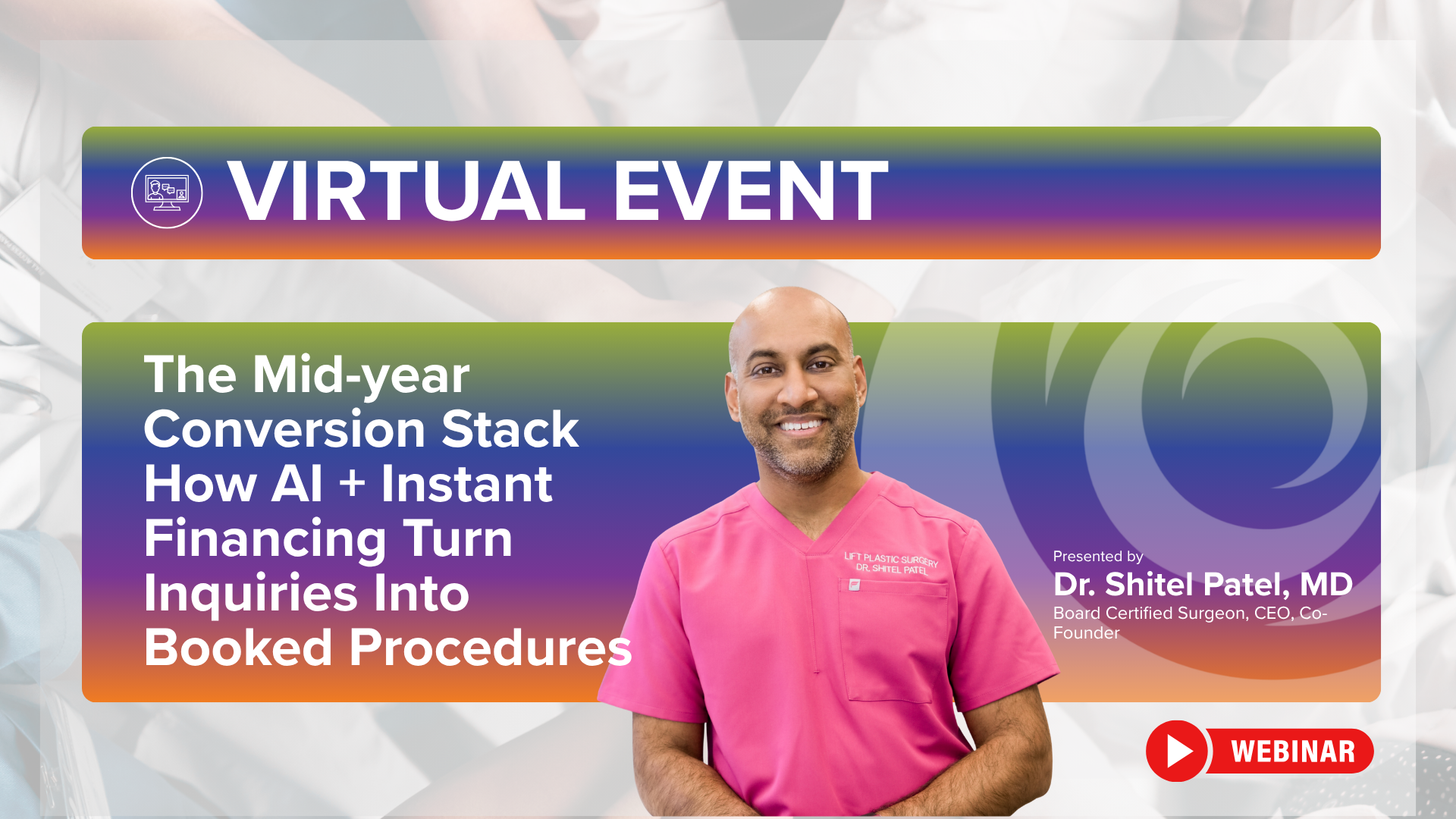

The Mid-year Conversion Stack How AI + Instant Financing Turn Inquiries Into Booked Procedures

What happens when you combine AI-powered patient engagement with instant patient financing?

More inquiries become consultations.

More consultations become booked procedures.

More patient interest turns into growth.

Join us on June 26 as Dr. Shitel Patel, MD, Board-Certified Surgeon, CEO, and Co-Founder of AdVital, shares how leading practices are leveraging AI and financing to improve conversion throughout the patient journey.

In this session, you'll learn:

✔ How AI is transforming speed-to-lead and patient engagement

✔ Why patients hesitate—and how to reduce decision friction

✔ How instant financing helps patients move forward with confidence

✔ Strategies to improve conversion without increasing acquisition costs

✔ What the modern "conversion stack" looks like for growth-focused practices

As patient acquisition costs continue to rise, the practices that win won't necessarily generate more leads—they'll convert more of the leads they already have.

📅 June 26

🕛 12:00 PM CST

Register today https://attendee.gotowebinar.com/register/8330973671364887648.

CareStack and Alphaeon Announce New Integration

New integration streamlines patient financing within CareStack's practice management platform, making it easier for providers to help patients move forward with care.

NEWPORT BEACH, Calif., June 23, 2026 /PRNewswire/ -- CareStack, a leading cloud-based dental practice management platform, and Alphaeon Patient Financing, a premier patient financing solution designed for elective healthcare, today announced the launch of a new integration that helps practices seamlessly incorporate patient financing into their existing workflows.

The integration is designed to address one of the most significant challenges facing healthcare providers today: helping patients confidently move forward with treatment in an environment where patient financial responsibility continues to rise.

"Financial concerns remain one of the biggest barriers between patients and treatment," said Abhi Krishna, Chief Executive Officer of CareStack. "By integrating Alphaeon into CareStack, we're helping practices make accessible financing part of the care journey, enabling more patients to move forward with recommended treatment, while improving case acceptance and practice growth for our customers."

By connecting CareStack's comprehensive practice management capabilities with Alphaeon's financing platform, providers can offer patients flexible payment options directly within their workflow, reducing financial friction, improving operational efficiency, and increasing treatment acceptance.

"Patients are increasingly seeking flexible ways to pay for care, and providers need tools that make those conversations easier," said Thomas Ervesun, Chief Executive Officer, Alphaeon. "By integrating Alphaeon directly within CareStack, we're helping practices remove barriers that often stand between patients and treatment. Together, we're creating a better experience for providers, staff, and the patients they serve."

Addressing a Growing Industry Challenge

As deductibles, out-of-pocket expenses, and elective treatment costs continue to rise, financial concerns have become one of the leading reasons patients delay or decline recommended care.

For practices, this often results in:

Lower case acceptance rates

Delayed treatment starts

Lost production opportunities

Increased pressure on front-office teams

Slower revenue growth

The new CareStack and Alphaeon integration helps practices proactively address these challenges by making financing more accessible, visible, and actionable at the point of care.

Key Benefits of the Integration

The integration enables practices to:

Present financing options within existing workflows

Reduce administrative burden on clinical and front-office teams

Help patients make informed treatment decisions with confidence

Improve treatment conversion and case acceptance rates

Increase revenue opportunities through higher treatment completion

Deliver a more convenient and patient-friendly financial experience

Supporting Practice Growth Through Better Financial Experiences

The integration reflects a growing trend among leading healthcare organizations: recognizing that patient financing is no longer simply a payment solution, but a strategic growth tool.

When patients have access to financing options that fit their needs, providers can help more patients move forward with treatment plans, improve patient satisfaction, and strengthen practice performance.

With Alphaeon's industry-leading provider support, competitive financing offers, and patient-first approach combined with CareStack's modern cloud-based platform, practices now have a powerful solution to help drive both operational efficiency and practice growth.

Availability

The CareStack and Alphaeon integration is now available to eligible CareStack customers.

To learn more about the integration and upcoming educational opportunities, visit myalphaeoncredit.com/carestack.

About CareStack

CareStack is a leading cloud-based dental practice management platform designed to simplify operations, improve patient engagement, and help dental organizations scale efficiently. Its all-in-one platform supports scheduling, clinical workflows, billing, analytics, patient communications, and more for practices of all sizes.

About Alphaeon

Alphaeon is a patient financing solution that helps patients access elective healthcare procedures and treatments through flexible payment options. Trusted by providers nationwide, Alphaeon helps practices improve patient affordability, increase treatment acceptance, and support long-term growth backed by a 24/7 provider-hotline answered in 60 seconds or less. Learn more about our provider solutions at myalphaeoncredit.com.

CareStack Customer Exclusive

Unlock More Growth with the New Alphaeon Integration

Your practice already relies on CareStack to streamline operations, improve efficiency, and deliver a better patient experience.

Now it's time to unlock even more growth.

Join CareStack and Alphaeon on June 23rd for an exclusive customer webinar showcasing the newest CareStack–Alphaeon Patient Financing integration and how practices are using it to remove financial barriers, increase treatment acceptance, and make financing easier than ever for both patients and staff.

Why You Can't Afford to Miss This

Every day, patients leave treatment plans undecided—not because they don't want care, but because they're unsure how they'll pay for it.

The result?

Delayed treatment

Lower case acceptance

Lost production

Missed revenue opportunities

The new CareStack and Alphaeon integration helps solve this challenge by embedding financing directly into your workflow, making it easier for your team to present options, support patient decisions, and help more patients move forward with treatment.

What This Integration Unlocks for Your Practice

✔️ Higher case acceptance and treatment conversion

✔️ Faster, more confident patient decisions

✔️ Improved cash flow and production growth

✔️ Less administrative burden on your team

✔️ A seamless workflow between practice management and financing

✔️ Better patient experiences with flexible payment options

When financing becomes easier to present and easier for patients to access, more treatment plans become completed treatment—and that's where real growth happens.

What You'll Learn

How patient financing directly impacts practice growth, revenue, and cash flow

Where practices lose patients due to financial uncertainty—and how to prevent it

How the new integration simplifies financing conversations inside your existing CareStack workflow

Best practices for increasing case acceptance without creating pressure for patients

What makes Alphaeon different, including competitive offers, higher approval opportunities, and dedicated provider support

Featuring Experts from CareStack & Alphaeon

Hear directly from leaders at both organizations as they demonstrate how practices are connecting operations and financing to create a more seamless—and more profitable—patient journey.

Bonus for Attendees

Join us live and we'll treat you to:

☕ Coffee on us — Every attendee receives a coffee gift card

🍽️ Chance to Win a $300 Summer Team Lunch — One lucky practice will receive a catered lunch for their team

This is more than a product update.

It's an opportunity to learn how to help more patients say yes, support your team with better tools, and unlock additional growth from the patients already walking through your doors.

Register now and discover what's possible with the newest CareStack–Alphaeon integration.

We look forward to seeing you on June 23rd!

The CareStack & Alphaeon Teams

The Summer Slowdown Is Coming: How Patient Financing Can Protect Your Practice Revenue

Every practice owner knows the pattern. As temperatures rise and vacation season kicks in, appointment calendars start showing gaps. Patients postpone elective procedures, delay treatment plans, and prioritize family trips over follow-up visits. The summer slowdown is a predictable challenge—but it doesn't have to mean predictable revenue losses.

What many practices overlook during slower months is that patient hesitation often isn't about timing at all. It's about money. The family vacation competing with that cosmetic procedure? The summer camp tuition that's bumping the LASIK consultation? These aren't necessarily either/or decisions—not when patients have access to flexible payment options that let them manage both.

Here's how strategic patient financing can transform your practice's summer from a revenue valley into surprisingly strong months.

The Psychology Behind Summer Postponement

When patients delay treatment during summer months, they rarely articulate the real reason. They'll mention busy schedules, travel plans, or wanting to "wait until fall." But dig deeper, and a financial calculation is almost always at play.

Summer brings concentrated expenses for many households: vacations, camp fees, back-to-school shopping on the horizon, home improvement projects. These competing demands make large out-of-pocket healthcare expenses feel particularly burdensome—even for patients who could technically afford them.

The key insight? Many of these patients aren't saying "no" to treatment. They're saying "not right now, not all at once." That's a fundamentally different objection, and it's one that patient financing directly addresses.

Reframing the Conversation

Consider how the treatment acceptance conversation typically unfolds:

Without financing: "The total for your treatment plan is $4,500. How would you like to pay?"

The patient mentally calculates that $4,500 against summer expenses, feels the weight of the number, and says they'll "think about it" or "schedule after Labor Day."

With financing presented upfront: "Your treatment plan totals $4,500. Many of our patients find it easier to manage this as monthly payments—often under $150 per month with our financing options. Would you like to see what you'd qualify for? It takes about two minutes and won't affect your credit score."

Now the patient is comparing $150 per month against their budget, not $4,500. That's a fundamentally different mental calculation—and one that often leads to "yes, let's do it now."

Why Summer Is Actually Ideal for Many Procedures

Here's what your front desk team should be communicating: summer can actually be the better time for many elective procedures.

Recovery time: Patients with flexible summer schedules—teachers, students, parents coordinating around school calendars—may have more time to recover than they will during the busy fall.

Advance booking advantage: Scheduling now means securing preferred appointment times before the fall rush when everyone who "waited until after summer" calls at once.

Results timing: Patients who want to look their best for fall events, holiday photos, or year-end celebrations need to start treatment now.

Promotional opportunities: Summer slowdowns create opportunities for practices to offer promotional financing terms that might not be available during peak seasons.

Patient financing transforms summer's perceived disadvantage—competing expenses—into an actual advantage: payments spread over time align beautifully with patients who have more time for recovery.

Proactive Outreach to Pending Treatment Plans

Most practices have a list of patients who received treatment recommendations but haven't scheduled. Summer is the perfect time to revisit these conversations with a financing-forward approach.

Consider outreach messaging like:

"Hi [Patient Name], I'm reaching out from [Practice Name] about the treatment we discussed back in [month]. I wanted to let you know that we now have some flexible payment options that many patients are finding really helpful. If budget was a factor in your decision to wait, I'd love to share what's available—there's no obligation, and checking won't affect your credit score. Would you have a few minutes to talk this week?"

This approach does several things: it acknowledges (without assuming) that cost may have been a factor, it introduces a solution, and it removes the perceived risk of exploring options.

Training Your Team for Summer Success

Your front desk and treatment coordinators are the difference between financing being utilized and financing being forgotten. Summer is an excellent time to invest in training that ensures your team:

Introduces financing early. Patients should hear about payment options before they see final numbers—not as a last resort after sticker shock has set in.

Normalizes the conversation. Language matters. "Would you like to apply for financing?" sounds remedial. "Would you like to see your monthly payment options?" sounds helpful.

Understands the approval process. Team members confident in explaining soft credit checks, approval timelines, and payment structures will present financing more naturally.

Follows up effectively. Patients who check their options but don't proceed immediately should receive thoughtful follow-up—not aggressive sales pressure, but genuine check-ins.

Alphaeon Credit offers training resources and ongoing support specifically designed to help practice teams become comfortable and confident with patient financing conversations. Summer's slower pace makes it the ideal time to invest in this training.

Leveraging Multiple Financing Tiers

Not every patient has the same credit profile, and single-tier financing solutions leave money on the table. Practices partnering with financing providers that offer multiple approval tiers—from prime to near-prime to subprime—capture cases that would otherwise walk out the door.

With multi-tier solutions like those offered through Alphaeon Credit, a single application can match patients with the financing option best suited to their credit profile. More approvals mean more scheduled procedures, more revenue, and more patients receiving the care they need.

During summer months, when every case matters more to your bottom line, these expanded approval rates become particularly valuable.

Marketing Financing Proactively

Don't wait for patients to ask about payment options. Make financing part of your summer marketing:

Website visibility: Ensure payment options are prominently featured, not buried in a FAQ page. Patients researching your practice should immediately see that flexible payments are available.

Social media: Posts highlighting payment plan availability normalize the conversation before patients ever contact you.

Email campaigns: Reach out to your patient base with messaging focused on accessibility: "Great care shouldn't require waiting. Ask about our flexible payment plans."

In-office signage: Counter cards, posters, and waiting room materials should remind patients that options exist.

Consultation integration: Treatment coordinators should present financing as a standard part of every consultation, not a fallback.

Alphaeon Credit provides marketing materials and resources to help practices communicate financing availability effectively across all these channels.

The Math That Matters

Consider the real impact of converting even a few "I'll wait until fall" responses into "Let's move forward now" decisions:

If your average elective procedure generates $3,000 in revenue, converting just four additional patients per month through financing availability represents $12,000 in monthly revenue that would have otherwise been delayed—or lost entirely to a competitor who made payment easier.

Over a three-month summer period, that's $36,000 in revenue protected. And because those patients are now in your active treatment cycle, they're also more likely to return for maintenance, follow-up, and additional services.

Building Year-Round Financial Accessibility

The strategies that protect summer revenue don't stop working when fall arrives. Practices that build patient financing into their standard operations see benefits throughout the year:

Higher case acceptance rates across all seasons

Larger average transaction sizes (patients pursue comprehensive treatment plans when monthly payments are manageable)

Improved patient satisfaction (financial flexibility reduces stress and improves the overall care experience)

Competitive differentiation (patients increasingly expect payment options)

Reduced accounts receivable challenges (financing partners pay the practice while patients pay over time)

Summer may be the catalyst for integrating financing more deeply into your practice, but the benefits compound year after year.

Partner With Alphaeon Credit

For over a decade, Alphaeon Credit has helped healthcare practices turn financial obstacles into treatment acceptance. Our platform is built specifically for elective healthcare—dental, vision, aesthetics, audiology, veterinary, and beyond—with features designed around how these practices actually operate.

With credit lines up to $25,000, multi-tier approval options that expand your approval spectrum, and a dedicated practice support hotline answered by real people (not phone trees), Alphaeon Credit partners with your team to make financing work for your patients and your practice.

Enrollment is free, setup is fast, and training is available to ensure your team is confident from day one.

Don't let summer become a revenue gap. Visit myalphaeoncredit.com/get-started to enroll your practice, or call our practice support team to learn more about how patient financing can transform your seasonal revenue patterns.

Turning “I’ll Think About It” Into Yes: AADOM Quickcast with Alphaeon

“I’ll think about it.”

Few phrases are more familiar—or more frustrating—for dental and elective healthcare practices.

The patient seemed interested. They asked thoughtful questions. They agreed they wanted the procedure. But when it came time to move forward, hesitation took over.

For many practices, this moment is often viewed as a sales challenge or a lack of urgency from the patient.

In reality, it’s usually something much deeper: uncertainty.

A New Reality in Patient Decision-Making

Today’s patients are navigating rising healthcare costs, economic pressure, and more financial responsibility than ever before.

They’re not just evaluating treatment recommendations—they’re evaluating whether they feel emotionally and financially confident enough to move forward.

And that’s changing everything about case acceptance.

What used to be a straightforward clinical decision is now:

A financial decision

A trust-based decision

A confidence-based decision

For dental teams, this shift requires a new approach.

A Partnership Focused on What Matters Most

As part of our ongoing partnership with AADOM (American Association of Dental Office Management), Alphaeon Patient Financing is proud to feature an upcoming Quickcast session with Tate Roark, VP of Dental Enterprise at Alphaeon: https://www.dentalmanagers.com/blog/aadom-quickcast-why-patients-say-ill-think-about-it-and-how-practices-can-help-patients-say-yes/

Why Patients Say “I’ll Think About It”—And How Practices Can Help Patients Say Yes

This session is designed specifically for dental office managers and team leaders who are navigating these challenges every day.

Together, we’ll explore what’s really happening in that moment of hesitation—and how practices can respond in a way that supports both the patient and the business. Join us May 26th at 2:00p CST at https://www.dentalmanagers.com/blog/aadom-quickcast-why-patients-say-ill-think-about-it-and-how-practices-can-help-patients-say-yes/.

Positioning Financial Conversations with Confidence

Specialty procedures are some of the most valuable—and most difficult—to convert.

Higher costs. Greater complexity. Longer decision timelines. Even when patients need the treatment, hesitation is common—and too often, cases stall.

In this session, Angelique Swann, Director of Provider Performance Enablement at Dental Care Alliance, brings a powerful, real-world perspective on how leading organizations are improving case acceptance in complex, high-value care environments. Drawing on her experience supporting more than 900 providers and 500 practices, as well as her work across implant dentistry, DSOs, and global healthcare organizations, Angelique will break down the key barriers that impact patient decision-making—and how to overcome them.

What You’ll Learn

Why specialty and high-ticket procedures create unique challenges in case acceptance

The psychology behind patient hesitation—and how to address it effectively

How to position financial conversations with clarity and confidence

Strategies to build trust, reduce uncertainty, and guide patients to decisions

Practical approaches to improving conversion without pressure or discounting

Register Now

About the Presenter

Angelique Swann serves as the Director of Provider Performance Enablement at Dental Care Alliance, where she helps optimize, strengthen, and grow more than 900 dental providers and 500 dental practices across the organization. Her work focuses on driving provider performance, accelerating growth, and creating measurable impact through strategic enablement, education, and operational excellence. With consulting experience alongside respected firms such as Pritchett & Associates and Dick Grote’s Performance Systems Corporation, Angelique brings a diverse background spanning pharmaceuticals, biotechnology, medical devices, and implant dentistry. This breadth of experience has shaped her deep understanding of provider behavior, patient decision-making, and the psychology behind successful treatment acceptance—particularly within complex, high-value care environments.

As a coach, speaker, and educator, Angelique developed her expertise in dental instructional design and provider performance while working with industry leaders including ClearChoice Dental Implant Centers, Nobel Biocare, and Straumann Group. She has partnered with manufacturers, DSOs, and private practices throughout the United States, Europe, and the Middle East, helping teams drive sustainable growth and improve business performance. Angelique is particularly passionate about equipping providers and teams with the skills needed to position financial conversations with confidence, increase case acceptance, and successfully navigate the unique challenges that often accompany specialty and high-ticket procedures. Her work emphasizes helping clinicians and teams create clarity, certainty, and trust—transforming difficult conversations into opportunities for better patient outcomes and practice growth. Angelique is committed to helping organizations build productive, profitable, and high- performing cultures that elevate both the provider and patient experience.

Fear, Finances & Follow-Up: The 3 Biggest Factors Impacting Elective Procedure Conversion

Fear, Finances & Follow-Up: The 3 Biggest Factors Impacting Elective Procedure Conversion

In vision and cosmetic practices, patients aren’t just making clinical decisions—they’re making emotional and financial ones.

And too often, those decisions stall.

Patients hesitate. They delay. They say, “I’ll think about it.”

Not because they don’t want the procedure—but because something is getting in the way.

In this session, Dallas Logan, a seasoned growth leader across ophthalmology, aesthetics, and cash-pay practices, breaks down the three critical factors that determine whether a patient moves forward—or walks away:

👉 Fear – The emotional barriers that go unaddressed

👉 Finances – The uncertainty that creates hesitation

👉 Follow-Up – The missed opportunities after the consult

You’ll learn how leading practices are:

Addressing patient concerns with confidence and empathy

Presenting financial options in a way that builds trust—not pressure

Creating follow-up systems that re-engage and convert interested patients

Turning more consults into completed procedures—without discounting

The takeaway:

If you want to increase conversion in elective care, you don’t need more consults—you need a better strategy for what happens during and after them.

This session will give you practical, proven ways to help more patients move forward with confidence—while driving meaningful growth for your practice.

In vision and cosmetic practices, patients aren’t just making clinical decisions—they’re making emotional and financial ones.

And too often, those decisions stall.

Patients hesitate. They delay. They say, “I’ll think about it.”

Not because they don’t want the procedure—but because something is getting in the way.

In this session, Dallas Logan, a seasoned growth leader across ophthalmology, aesthetics, and cash-pay practices, breaks down the three critical factors that determine whether a patient moves forward—or walks away:

👉 Fear – The emotional barriers that go unaddressed

👉 Finances – The uncertainty that creates hesitation

👉 Follow-Up – The missed opportunities after the consult

You’ll learn how leading practices are:

Addressing patient concerns with confidence and empathy

Presenting financial options in a way that builds trust—not pressure

Creating follow-up systems that re-engage and convert interested patients

Turning more consults into completed procedures—without discounting

The takeaway:

If you want to increase conversion in elective care, you don’t need more consults—you need a better strategy for what happens during and after them.

This session will give you practical, proven ways to help more patients move forward with confidence—while driving meaningful growth for your practice.

REGISTER NOW

The Hidden Cost of "We'll Bill You Monthly": Why In-House Payment Plans Are Draining Your Practice

It seems like a patient-friendly solution: when a patient can't pay in full, your practice offers to bill them monthly. No outside financing, no applications, just a handshake agreement and a series of invoices.

What could go wrong?

As it turns out, quite a lot. In-house payment plans carry hidden costs that most practices never fully calculate—costs that drain staff time, strain cash flow, create collection headaches, and ultimately harm the patient relationships they were meant to protect.

April is a natural time for practices to evaluate operations and clean up processes that aren't serving them. If your practice is managing internal payment plans, here's what that decision is really costing you.

The Cash Flow Problem You're Creating

When a patient pays in full—whether with cash, credit card, or third-party financing—your practice receives the revenue immediately (or within a few business days for financing). That money is available for payroll, supplies, rent, and growth investments.

When you offer in-house payment plans, that same revenue trickles in over months or years. A $6,000 treatment plan billed at $500/month takes a full year to collect—assuming every payment arrives on time, which they rarely do.

The cash flow implications compound quickly:

Working capital strain: Money you've earned but haven't collected can't be used. Practices with significant receivables tied up in payment plans often face cash crunches despite being technically profitable.

Growth limitations: Expansion, equipment purchases, and hiring require capital. When that capital is sitting in patient payment plans, growth stalls.

Increased borrowing: Some practices end up taking on debt to cover operating expenses while waiting for payment plan installments—essentially borrowing money because they lent money to patients.

Third-party financing eliminates this problem entirely. The financing company pays your practice upfront (typically within 48-72 hours), and the patient's payment relationship is with the lender, not with you. Your cash flow remains predictable and immediate.

The Administrative Burden Nobody Accounts For

Managing payment plans requires work—more work than most practices realize when they first offer them.

Consider everything involved:

Invoicing: Someone must generate and send monthly statements. Even with automated systems, this requires setup, maintenance, and oversight.

Payment processing: Payments must be recorded, reconciled, and deposited. When patients pay by check, someone handles physical deposits. When they pay by card, fees apply.

Follow-up on late payments: This is where the real time drain begins. When payments don't arrive, someone must call, email, or send reminders. These conversations are uncomfortable and time-consuming.

Account management: Patients call with questions, request payment date changes, dispute charges, or ask for modifications. Each interaction requires staff time.

Collections escalation: When patients stop paying entirely, practices face a choice: write off the balance, send to collections (damaging the patient relationship), or continue pursuing payment internally (consuming more staff resources).

Now multiply this by dozens or hundreds of active payment plans. The administrative burden becomes a significant hidden expense—staff hours that could be spent on patient care, scheduling, or other revenue-generating activities.

With third-party financing, the administrative burden shifts entirely to the financing partner. Your practice processes one transaction at the time of service; everything else is handled by the lender.

The Collections Reality

Here's the uncomfortable truth about in-house payment plans: a meaningful percentage of patients don't complete their payments.

Industry data suggests that practices managing their own payment plans experience default rates significantly higher than third-party financing—sometimes 15-20% or more, depending on payment plan terms and patient demographics.

When a patient defaults on a third-party financing agreement, the practice has already been paid. The loss belongs to the financing company, not to you.

When a patient defaults on an in-house payment plan, the practice absorbs the loss directly. That $6,000 treatment plan where the patient paid three installments and disappeared? You've collected $1,500 and written off $4,500.

Some practices turn to collection agencies for delinquent accounts, but this introduces additional costs (agencies typically keep 25-50% of collected amounts) and risks damaging patient relationships permanently.

Others simply write off bad debt as a cost of doing business—but that cost is rarely calculated accurately when deciding whether to offer payment plans in the first place.

The Patient Relationship Risk

In-house payment plans position your practice as a creditor to your patients. This fundamentally changes the relationship dynamic.

When a patient falls behind on payments:

Your team must have uncomfortable conversations about money

The patient may feel embarrassed or resentful

The patient may avoid scheduling needed follow-up care to escape payment discussions

The patient may leave negative reviews based on billing conflicts rather than clinical care

The relationship becomes transactional rather than therapeutic

These dynamics are particularly damaging in practices that depend on long-term patient relationships—dental offices, dermatology practices, aesthetic clinics, and others where ongoing care and referrals drive growth.

Third-party financing creates separation between clinical care and payment. If a patient has questions or issues with their financing, they contact the financing company—not your front desk. Your team remains focused on care, and the patient relationship stays intact regardless of payment circumstances.

Calculating the True Cost

Most practices that offer in-house payment plans have never calculated the true cost. Here's a framework:

Staff time: Estimate hours spent monthly on invoicing, payment processing, follow-up, and account management. Multiply by loaded labor cost (wages plus benefits). For many practices, this easily exceeds $1,000-2,000 monthly.

Bad debt: Calculate the dollar value of payment plans that were never completed over the past year. This is pure revenue loss.

Opportunity cost of delayed cash flow: What could your practice have done with the capital tied up in receivables? This is harder to quantify but very real.

Collections costs: If you use collection agencies, what have you paid them? What have they actually recovered?

Relationship costs: How many patients have you lost due to payment conflicts? What's the lifetime value of those relationships?

When practices actually run these numbers, they're often shocked. The "free" solution of billing patients monthly frequently costs more than third-party financing fees would have.

The Financing Fee Objection

The most common reason practices give for avoiding third-party financing: "We don't want to pay the fees."

Third-party financing does involve merchant fees—typically a percentage of the financed amount. This feels like a direct cost that in-house payment plans avoid.

But this framing ignores everything outlined above:

In-house plans have administrative costs (staff time)

In-house plans have bad debt costs (defaults)

In-house plans have opportunity costs (tied-up capital)

In-house plans have relationship costs (patient conflicts)

When all costs are accounted for, third-party financing fees often represent a savings compared to in-house payment plans, not an expense.

Moreover, practices using financing typically see higher case acceptance rates. Patients who might not commit to a payment plan with your practice—concerned about the relationship implications or uncertain about their own follow-through—often feel more comfortable with formal financing through an established lender.

Higher case acceptance means more revenue. Even if financing fees were a net cost (which they often aren't), increased volume frequently more than offsets them.

Making the Transition

If your practice currently manages in-house payment plans, transitioning to third-party financing doesn't have to be abrupt:

For new treatment plans: Begin offering third-party financing as the standard option. Reserve in-house arrangements for exceptional circumstances only.

For existing payment plans: Continue managing current plans to completion, but don't add new ones. Your receivables will naturally wind down over time.

For patient communication: Position the change positively: "We've partnered with a financing provider that offers more flexible options and makes the payment process easier for our patients."

Most patients prefer financing through established providers anyway—it feels more formal, more structured, and more separate from their healthcare relationship.

Partner With Alphaeon Credit

For over a decade, Alphaeon Credit has helped practices escape the in-house payment plan trap. Our platform delivers the patient flexibility of payment plans with none of the administrative burden, cash flow strain, or collection risk.

With credit lines up to $25,000, multi-tier approvals that expand your acceptance rates, and promotional financing options that patients prefer, Alphaeon Credit transforms how your practice handles treatment financing.

You get paid within days of service. Patients get manageable monthly payments. Your staff gets to focus on care instead of collections.

Stop managing payment plans that drain your resources. Visit myalphaeoncredit.com/get-started to enroll your practice, or contact our team to discuss how third-party financing can improve your cash flow, reduce administrative burden, and protect patient relationships.

The New Payer at the Table: How Patient Financial Responsibility is Reshaping Revenue Cycle

The Patient Is Now Your Biggest Payer—Is Your Revenue Cycle Ready?

Healthcare is undergoing a fundamental shift. Patients are no longer responsible for just a copay—they’re becoming one of the largest financial stakeholders in the care journey. And yet, most practices are still operating with revenue cycle processes built for a payer-driven world. In this session, we’ll explore how the rise of patient financial responsibility is reshaping the revenue cycle—and what that means for your practice.

You’ll learn:

How increasing patient portion is impacting revenue, cash flow, and conversion

Where traditional revenue cycle models are breaking down

Why financial conversations are now critical to the patient experience

How leading practices are adapting to support patients while driving growth

The takeaway: If patients are now your largest payer, your strategy needs to evolve.

This session will show you how to better support patients—while strengthening your financial performance.

REGISTER NOW

About the Presenter

Cissy Mangrum, MBA, CMPE, CPC, CDC, is a nationally recognized healthcare operations strategist and revenue cycle authority with 25+ years of experience spanning both medical and dental environments. As Co-Founder, CRO, and CRMCO of RevTech Partners and MaximizeRCM Consulting, she leads a mission to disrupt the industry with platforms that elevate both patient care and revenue operational experience. Having worked with over 2,700 physicians and doctors in the U.S in the last 25 years. Cissy's conviction is clear: the differentiator is never the regulations; it is always the people and the systems. She is the host of The Hidden Pulse with Cissy and a forthcoming author of The Revenue Advantage.

The State of Patient Financing: What 500 Patients Are Telling Us

New research reveals how cost uncertainty is impacting care decisions—and what practices can do to improve access and increase case acceptance.

Patients Are Ready for Care—But Cost Is Holding Them Back

Today’s patients aren’t just evaluating treatment—they’re evaluating affordability.

Our latest survey of 500 consumers highlights a growing access gap:

A majority have experienced difficulty paying for care

Many delay or avoid treatment due to financial concerns

Most are actively looking for better payment solutions

Without clear financial options, even high-intent patients hesitate to move forward. Download the full report.

What This Means for Your Practice

This isn’t just patient behavior—it’s a growth opportunity.

Practices that proactively introduce financing:

Increase case acceptance

Reduce treatment delays

Improve patient experience

Unlock revenue from existing demand

The difference isn’t more leads—it’s better access.

Ready to Take the Next Step?

See how Alphaeon can help your practice improve patient access and increase case acceptance.

Enroll in minutes—at no cost

Offer flexible financing options to your patients

Join a growing network focused on expanding access to care

Get started here.

Stop the Denials. Win the Appeals: A proven approach to getting insurance to pay—without endless follow-up

Insurance issues are not random. They are system failures.

In this direct, tactical session, Ashley Bond breaks down the real difference between rejections, denials, and appeals and shows you how to fix the breakdown at its source. Instead of rewriting the same appeals over and over, you will learn how to identify the patterns behind denials, strengthen documentation before submission, and build a repeatable appeal process that produces results.

This course moves beyond reactive claim chasing and into structured revenue control. Attendees will walk away with a clear framework to reduce denials, increase collections, and create accountability across clinical, front office, and billing teams.

Denied is a status. Paid is the goal.

Learning Objectives

By the end of this course, participants will be able to:

Clearly differentiate between rejections and denials and identify where each occurs in the claim life cycle.

Identify root cause patterns behind common denial categories including documentation gaps, coding errors, frequency limitations, and coordination of benefits issues.

Implement a structured claim tracking and status note system that improves accountability, follow-up efficiency, and speed of payment.

Turn appeals into a structured process instead of a guessing game.

REGISTER NOW

About the Presenter

Ashley Bond is the co-founder and Chief Dental Billing Officer at Wisdom. With a background rooted in hands-on dental practice operations, she began her career working alongside her father in his dental practice, gaining real-world insight into the financial and operational challenges dental teams face every day. Ashley is a trusted advisor to dental practices nationwide, specializing in revenue cycle oversight, billing performance analysis, and leadership-level financial clarity. She is a frequent national speaker, presenting at major industry events including the Greater New York Dental Meeting (GNYDM) and the Chicago Midwinter Meeting, and is known for delivering practical, data-driven education that teams can implement immediately. In addition to her speaking work, Ashley is a contributor to leading dental industry publications, including Dental Economics, Inside Dentistry, and Dr. Bicuspid, where she shares actionable insights on billing performance, insurance strategy, and operational sustainability.

Why Financial Education Is Becoming Essential to Patient Access in Hearing Care

As the hearing care industry continues to evolve, one thing is becoming increasingly clear: clinical excellence alone is no longer enough to drive patient outcomes.

At AAA 2026 in San Antonio, this shift is front and center.

From conversations on the show floor to educational sessions like Dr. Amyn Amlani’s “The Economics of Hearing Care: Why Financing Has Become Essential to Patient Access,” there’s a growing recognition that access—not just awareness—is the defining challenge for providers today.

The Access Gap in Hearing Care

Patients today are more informed than ever about their hearing health—but that doesn’t always translate into treatment.

Why?

Because many are navigating:

Uncertainty around cost

Lack of clear financial expectations

Limited understanding of available options

The result is a familiar pattern:

Patients delay care, postpone decisions, or leave without moving forward—not because they don’t see value, but because they don’t feel confident in how to pay for it.

This is where the conversation is shifting.

Financial Education as a Clinical Enabler

Dr. Amlani’s session highlights an important truth:

Financial clarity is now a critical part of the patient experience—and a key driver of case acceptance.

When practices proactively educate patients on:

What treatment may cost

What options are available

How payments can be structured

They reduce uncertainty—and in doing so, they:

Increase patient confidence

Improve follow-through on care

Strengthen trust and long-term relationships

In other words, financial education isn’t separate from care—it’s part of it.

What We’re Seeing Across Practices

At Alphaeon, we work with practices across healthcare markets—including hearing care—and we consistently see the same pattern:

Practices that integrate financial conversations early and clearly:

See higher case acceptance

Reduce delays in treatment decisions

Create a smoother, more supportive patient experience

And importantly, they’re able to expand access to care for more patients—not just those who can pay upfront.

From Transaction to Access

The shift happening in hearing care is not just about offering financing—it’s about rethinking how access is delivered.

It means:

Moving from reactive conversations (“only if needed”)

To proactive education (“part of every patient journey”)

It means:

Making affordability visible early

Normalizing conversations around cost

Empowering patients to move forward with confidence

This is the foundation of a more modern, patient-centered experience.

Building a Network That Expands Access

As we connect with providers at AAA 2026, one thing is clear:

There is a growing desire to not just improve individual practices—but to build a broader ecosystem that supports patient access at scale.

That’s why we’re focused on growing a provider network that:

Supports better financial conversations

Helps practices increase case acceptance

Expands access to care across communities

Because when more providers are equipped to offer clear, flexible financial options, more patients can say yes to care.

Join the Movement Toward Better Access

If you’re attending AAA 2026, we invite you to:

Connect with the Alphaeon team onsite

Attend Dr. Amlani’s session

Be part of the conversation shaping the future of hearing care

And if you’re looking to take the next step:

Learn how your practice can enroll with Alphaeon in minutes—at no cost—and start expanding access for your patients.

Join a growing network of providers focused on delivering not just care—but confidence, clarity, and access.

The future of hearing care isn’t just about better technology.

It’s about making care more accessible, more understandable, and more achievable for every patient who walks through your door.

And that starts with education.

Learn More

How Patient Financing Works: A Guide to Increasing Case Acceptance and Improving Patient Access

In today’s healthcare environment, one of the biggest barriers to care isn’t awareness—it’s affordability.

Patients are more informed than ever about treatment options, whether in dental, audiology, aesthetics, or other elective care. But when it comes time to move forward, many hesitate due to cost concerns.

That’s where patient financing plays a critical role.

Understanding how patient financing works—and how to implement it effectively—can help practices increase case acceptance, improve patient experience, and expand access to care.

What Is Patient Financing?

Patient financing is a payment solution that allows patients to break the cost of treatment into manageable monthly payments instead of paying the full amount upfront.

With patient financing, patients can:

Apply quickly and securely

Access flexible payment options

Move forward with treatment without financial strain

For providers, offering financing helps remove one of the biggest obstacles in the patient decision-making process.

Why Patient Financing Is Essential for Patient Access

One of the most common reasons patients delay or decline treatment is uncertainty around cost.

Patients often ask:

“How much will this cost?”

“Can I afford this right now?”

“What are my payment options?”

Without clear answers, many patients postpone care—even when it’s needed.

By offering transparent healthcare financing options, practices can:

Reduce patient anxiety

Improve trust and communication

Help patients feel confident moving forward

This directly supports better patient access to care.

How Patient Financing Improves Case Acceptance

Practices that integrate financing into their workflow consistently see higher conversion rates.

Here’s why:

1. Patients Focus on Monthly Cost Instead of Total Cost

Breaking treatment into monthly payments makes care feel more achievable.

2. Financial Conversations Become Easier

Staff can confidently present options instead of avoiding cost discussions.

3. Decisions Happen Faster

When affordability is clear, patients are less likely to delay treatment.

4. More Patients Say Yes to Care

The result is improved case acceptance rates and increased production.

Best Practices for Offering Patient Financing

To maximize results, patient financing should be introduced proactively—not as a last resort.

High-performing practices:

Introduce financing before the visit (during scheduling)

Present it alongside treatment options

Reinforce it at checkout and follow-up

This ensures patients always understand their options.

Watch: How Patient Financing Works

Our animated explainer video walks through the process step-by-step and shows how financing supports both patients and providers.

🎥 Watch the video to see how Alphaeon Patient Financing works.

Why Patient Financing Drives Practice Growth

Patient financing isn’t just about payments—it’s a growth strategy.

Practices that offer flexible payment options benefit from:

Higher case acceptance

Reduced treatment delays

Improved patient satisfaction

Increased revenue without additional marketing spend

In many cases, the biggest growth opportunity isn’t more leads—it’s converting the patients you already have.

Make Patient Financing Part of Your Practice

Patient expectations are changing. Today’s patients want:

Transparency

Flexibility

Confidence in their decisions

Offering patient financing helps meet those expectations while supporting better outcomes for your practice.

Get Started with Alphaeon Patient Financing

Getting started is simple.

👉 Enroll your practice in minutes—at no cost—and start offering flexible payment options that improve patient access and increase case acceptance.

Join a growing network of providers using Alphaeon to deliver better patient experiences and drive sustainable growth.

Conclusion: Improving Access Starts with Affordability

Healthcare providers are focused on delivering the best possible care.

But without clear, accessible payment options, many patients won’t move forward.

By integrating patient financing into the patient journey, practices can:

Improve access

Increase acceptance

Deliver better outcomes

Because when patients can afford care, they’re more likely to receive it.

Learn More

Double Your Consults with the 7 Patient Archetypes

Learn How to Identify & Convert Every Caller with Customized Messaging

What you'll learn:

Every patient who calls your practice falls into one of 7 archetypes, and each one needs a completely different conversation to convert.

In this free training, Dr. Shitel Patel breaks down the framework he's used across 15,000+ procedures to identify caller type in under 30 seconds and match the message to what they actually need to book.

You'll walk away with:

• The 7 Patient Archetypes (with names that stick with your PCC's / Sales Staff)

• The signals that reveal each type in the first 30 seconds

• The conversion levers and the mistakes that kill the deal

• How to handle price objections before they derail the call

• LIVE demo: AI-powered sales role-play trainer

Presented by Ad Vital x Alphaeon Credit

About the Presenter

Dr. Shitel Patel, MD is a double board-certified plastic surgeon with fellowship training in craniofacial surgery from UT Southwestern and over 15,000 procedures performed at Lift Plastic Surgery in Houston, TX. He is also the CEO and co-founder of Ad Vital, an AI-powered CRM and practice management platform built specifically for aesthetic practices and medspas, born from the operational gaps he experienced running his own practice. Ad Vital's AI agents handle inbound calls, patient follow-up, and scheduling around the clock, helping practices convert more leads without adding headcount. A recognized voice on AI in aesthetic medicine, Dr. Patel has been featured on Doximity's Op-Med platform and the Outcomes Rocket podcast for his work on AI-driven patient acquisition and practice growth.

ACCESS RECORDING ON-DEMAND

Have Them at Hello: How Better Phone Conversations Drive Case Acceptance and Patient Trust

[WEBINAR EVENT] The patient experience doesn’t start in the treatment room—it starts on the first phone call. And in those first few minutes, patients are already deciding if they trust your practice and whether they’re going to move forward with care.

Most patients are calling with just two things on their mind: their insurance and their out-of-pocket cost. How your team handles those conversations—especially early—has a direct impact on case acceptance.

In this session, Laura Nelson will break down why phones are the first and most critical step in the case acceptance process, and how confidence, clarity, and consistency in communication can change everything. She’ll share practical strategies to help teams handle insurance and financial conversations in a way that builds trust instead of confusion.

Laura will also introduce how AI is starting to support the front desk—from ensuring calls are answered to helping keep patients engaged when teams are busy—and why this makes training your team on phone skills more important than ever.

Attendees will walk away understanding how to:

Create strong first impressions that build trust from the first call

Confidently guide conversations around insurance and finances

Keep callers engaged and reduce missed opportunities

Connect what happens on the phone to better treatment presentation and case acceptance

Use AI and technology as support—not a replacement—for great communication

This session will also introduce Laura’s phone training, giving teams a clear path to improving performance, consistency, and patient experience from the very first interaction.

About the Presenter

Laura Nelson is a nationally recognized speaker and dental industry expert with over 20 years of experience in dental practice operations. She is the founder of Front Office Rocks and currently serves as VP of AI, Training, and Development at Mango Voice, where she helps practices improve communication, efficiency, and patient experience through both proven systems and emerging technology. Laura is known for her practical, real-world approach to training teams—especially when it comes to phone skills, case acceptance, and creating consistency at the front desk.

REGISTER NOW

Paid in 30 Days — Mastering the Money Talk

[WEBINAR EVENT] Presented by Bri Richardson, Founder, Elevate My Practice and Dental Insurance SOS

How we think about money shapes how we talk about money — and patients feel it immediately. Paid in 30 Days: Mastering the Money Talk starts with mindset, because confident, clear financial conversations don’t come from scripts. They come from how your team understands money, insurance, and their role in the conversation.

This course helps dental teams confidently present treatment while getting paid in full from both insurance and patients. You’ll learn how to lead upfront, accurate financial conversations that build trust, set expectations clearly, and create a smoother experience for everyone involved — without the awkwardness or last-minute scrambling.

Through real treatment plan examples, you’ll see how having a solid insurance and financial game plan makes it easier to spot potential denials ahead of time and collect appropriately on the front end. Less chasing balances. Fewer uncomfortable follow-ups. Better outcomes.

This class brings the “money talk” to life by showing how money mindset, strong insurance systems, clear communication, and smarter treatment planning work together. When those pieces are aligned, the results are powerful: fewer misunderstandings, calmer patients, and healthier practice cash flow.

Key Learning Objectives

By the end of this course, participants will be able to:

Strengthen their money mindset and approach financial conversations with confidence

Clearly define the role of insurance in the financial discussion — without letting it run the conversation

Lead upfront conversations about treatment costs, insurance expectations, and patient responsibility

Spot potential insurance denials early to avoid delayed or lost collections

Confidently handle cost and insurance objections while maintaining trust

Clearly explain and offer third-party patient financing as a supportive solution

About the Presenter

Bri Richardson, Founder, Elevate My Practice and Dental Insurance SOS

Meet Bri Richardson, CDA, a vibrant force in the world of dental insurance! With her boundless enthusiasm and unwavering dedication to her craft, Bri shines as a dynamic Speaker, Coach, Dental Insurance Specialist, and Dental Team Trainer. She owns Elevate My Practice, LLC, and is the founder of Dental Insurance SOS.

Bri began her career as a dental assistant in 2009. Over the years, she has held various roles, from clinical assistant to treatment coordinator, and ultimately as a Dental Insurance Specialist, Speaker, Trainer, and Dental Coach. Bri has spent countless hours working on dental insurance claims and has mastered the art of extraordinary insurance verifications, perfect claim preparation, and overturning denials effectively. She is an expert at collecting the correct copays while navigating the red tape restrictions that can result in claim denials. As a speaker, Bri brings her expertise and contagious energy to help dental teams understand dental insurance and maximize their revenue while reducing their stress. She is the perfect advocate for teams looking to navigate the complex world of dental insurance and gain control of their A/R.

Bri began training dental teams how to get paid in 30 days and make insurance less painful in 2017. In 2021, she opened Elevate My Practice & Dental Insurance SOS and began training and speaking full time.

Elevate My Practice, LLC stands as a beacon of transformative training, offering both in-person and virtual sessions with CE. Recognizing the need for ongoing support, Bri introduced Dental Insurance SOS, providing dental teams with real-time assistance through text or email throughout their work day.

Bri's signature "micro-coaching" delivers focused guidance at an affordable price, offering accountability, KPI evaluation, monthly meetings, and continuous support for dentists and their teams.

Bri will be the first to tell you, she has the BEST job in the world. :)

ACCESS THE RECORDING

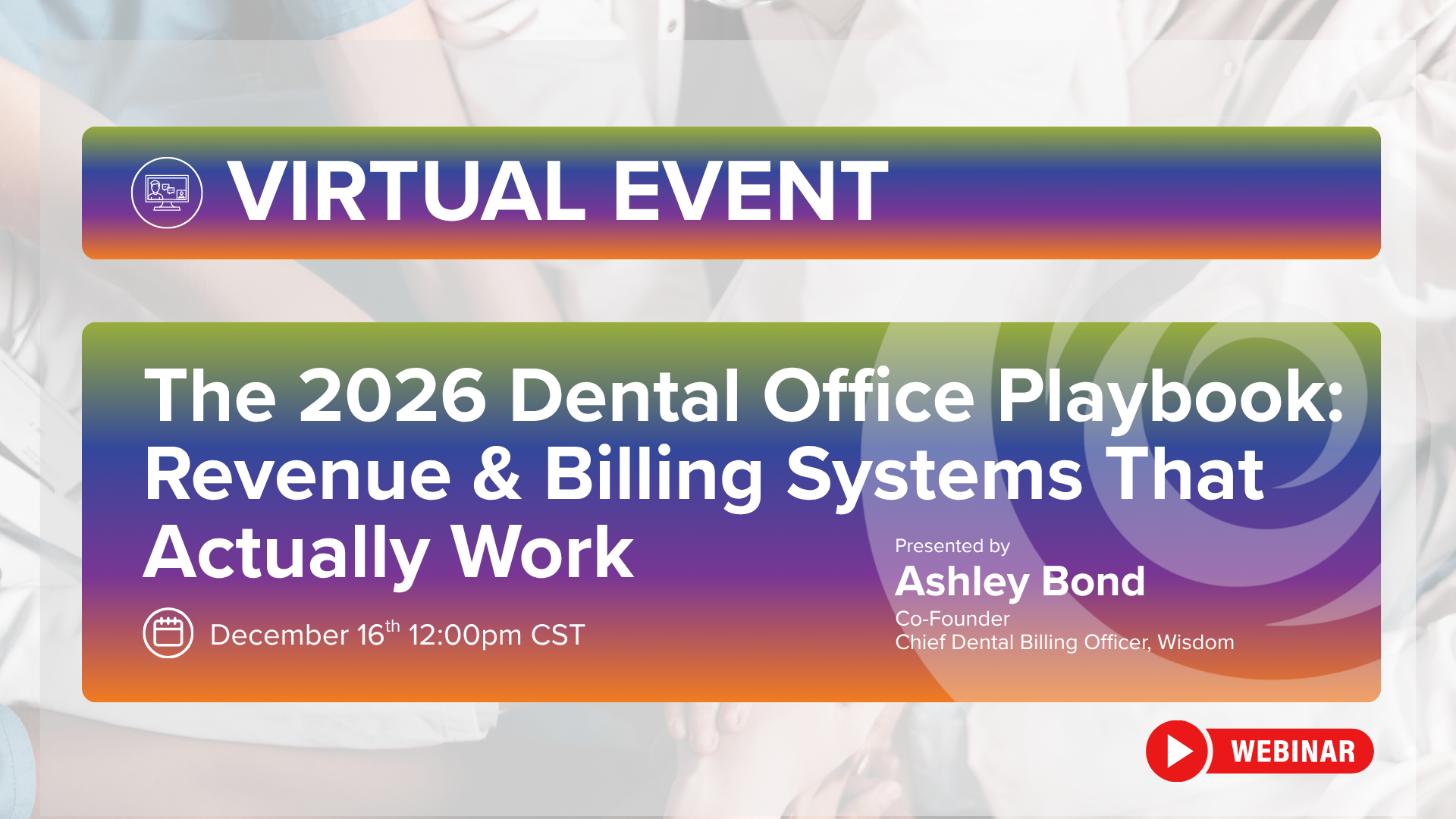

Webinar Event: The 2026 Dental Office Playbook- Revenue & Billing Systems That Actually Work

[WEBINAR EVENT] Today’s dental practices are fighting a revenue battle on multiple fronts—rising claim delays, inconsistent billing workflows, overwhelmed teams, and unpredictable cash flow. Most offices know their systems could run smoother… but few have the clarity, structure, and alignment needed to make it happen.

In The 2026 Dental Office Playbook: Revenue & Billing Systems That Actually Work, Ashley Bond, Co-Founder & Chief Dental Billing Officer at Wisdom, breaks down the proven operational and billing frameworks that top-performing practices rely on to protect revenue, reduce friction, and support scalable growth.

This session is designed for both emerging and established practices looking to streamline their operations, empower their teams, and finally take control of the revenue cycle. Whether you're a doctor, practice manager, front office leader, or billing specialist, you’ll walk away with practical steps you can implement immediately.

By the end of this webinar, attendees will be able to:

•• Identify operational and billing breakdowns that cause revenue loss in dental practices.

•• Understand how to implement consistent revenue & billing systems without overwhelming their teams.

•• Learn how to reduce insurance AR and claim delays while improving cash flow predictability.

•• Align front office, clinical, and billing teams around a unified revenue workflow.

•• Build scalable systems that reduce burnout and support sustainable growth.

About the Presenter

Ashley Bond, Wisdom Co-Founder & Chief Dental Billing Officer

Ashley Bond, Co-Founder & Chief Dental Billing Officer at Wisdom, leads our billing team, focusing on innovative solutions and training for enhanced service quality and efficiency. Previously, Ashley founded Bond Dental Billing, where she developed a nationwide billing service from her initial experience in her father's dental practice. Ashley is a proud member of the ASCA, SCN, demonstrating her commitment to professional development and excellence in the dental billing community. Ashley is passionate about continuing education in the dental community, and contributes in both editorial, and speaking capacities.

ACCESS THE RECORDING

Tax Season Is Your Practice's Hidden Opportunity: Why March Patients Are Ready to Say Yes

Every March, something shifts in your patients' financial mindset. Tax refunds hit bank accounts. Annual bonuses arrive. The fog of holiday spending finally clears. For elective healthcare practices, this window represents one of the most underutilized opportunities of the year.

But here's what most practices miss: the opportunity isn't just about patients who can suddenly pay in full. It's about patients who are thinking about money—evaluating their finances, making plans, and feeling more confident about commitments they've been postponing.

That mindset creates the perfect moment for patient financing conversations. Here's how to capitalize on tax season psychology to drive case acceptance in March and beyond.

The Tax Refund Reality Check

The average American tax refund hovers around $3,000. That's real money—enough to cover many elective procedures outright or make a significant dent in larger treatment plans.

But practices that expect patients to simply write checks from their refunds are missing half the picture.

Consider how patients actually think about their refunds:

Some earmark refunds for specific purposes before the money even arrives (debt payoff, savings, vacations)

Some receive refunds but face competing demands—home repairs, car maintenance, children's expenses

Some owe taxes rather than receiving refunds

Some receive refunds but prefer to keep cash reserves intact

In other words, a tax refund doesn't automatically translate to "ready to pay $4,000 out of pocket for cosmetic dentistry." What it does translate to is a patient who's actively engaged with their finances and more receptive to discussing payment options.

That's where financing enters the picture.

Why Tax Season Patients Respond to Financing

The psychological state of tax season makes patients particularly receptive to patient financing—even patients who could technically pay in full.

Financial awareness is heightened. Patients who just reviewed their entire year's finances are primed to think about budgeting and payment structures. Monthly payment options feel relevant because they're already thinking in those terms.

Confidence is elevated. A tax refund—or even just completing tax filing—creates a sense of financial control. Patients feel more confident about commitments, including treatment plans they've been considering.

The "fresh start" effect is real. Tax season aligns with new year energy that hasn't yet faded. Patients who set health or appearance goals in January are still motivated in March—and now they're thinking about how to fund those goals.

Comparison shopping is active. Patients evaluating whether to use their refund for procedures are also comparing practices. The practice that makes payment easiest often wins their business.

This combination of factors creates ideal conditions for financing conversations. Patients are ready to discuss money, confident about their ability to commit, and actively comparing their options.

Reframing the Refund Conversation

Your team's approach to tax season patients should acknowledge the financial moment without making assumptions.

Avoid: "Are you planning to use your tax refund to pay for this?"

This question puts patients on the spot and makes assumptions about their financial situation. It can feel intrusive.